Last months’s release of the “Big 6” proposal from Republican congressional leaders and the Trump Administration officially began the long-awaited debate over taxes. An oft-repeated claim in this debate is that high American corporate income tax rates harm American workers by rendering our corporations less “competitive” globally. Let us be really clear about this: Such a claim is pure economic snake-oil.

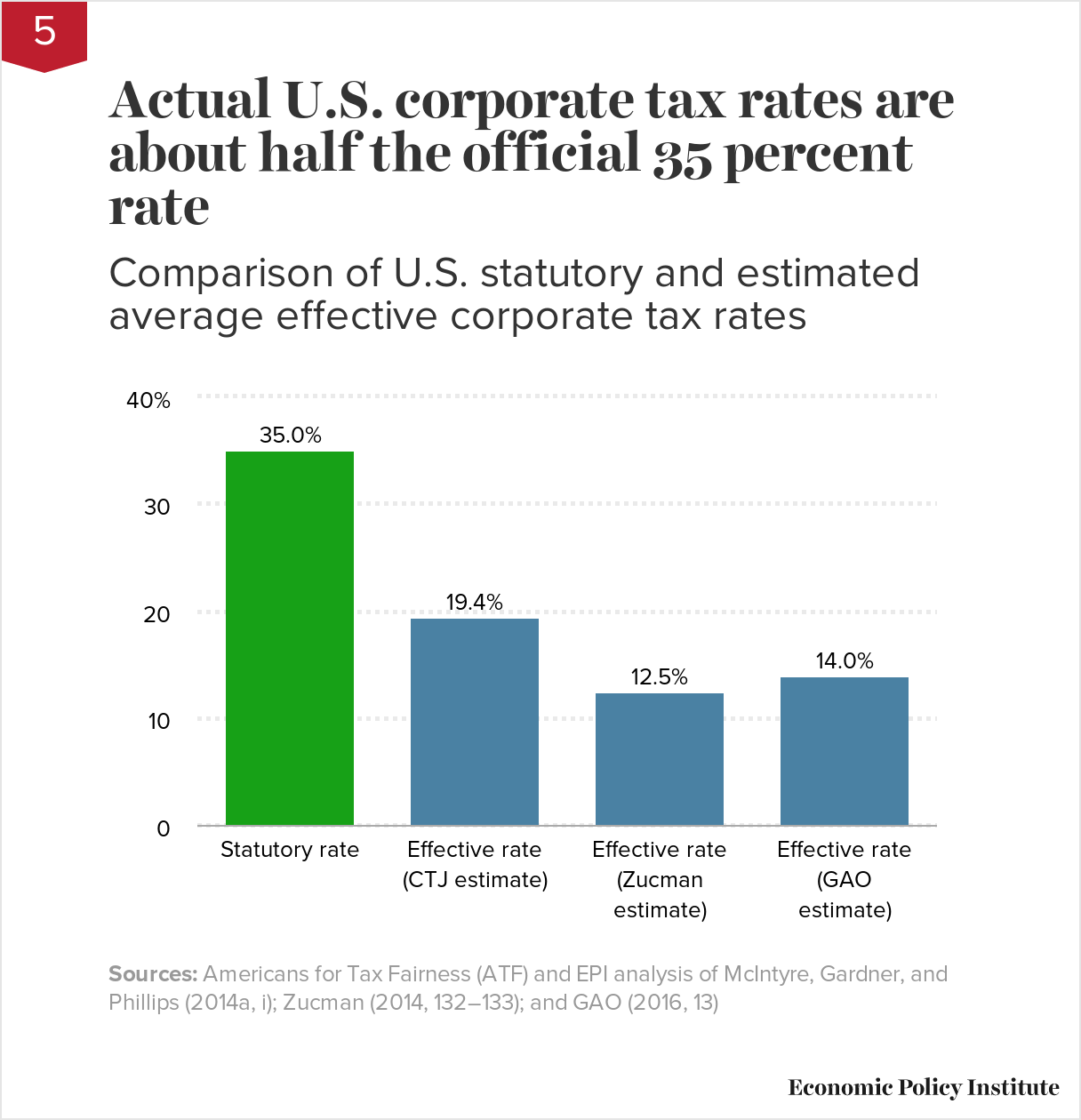

For one thing, the real-world evidence is clear that while the statutory rate that U.S. corporations are supposed to pay (35 percent) is higher than our industrial peers, the effective rate that these corporations actually pay after their accountants get involved is firmly in line with these peers (estimates vary a bit, but most have the effective rate in the U.S. hovering around the low 20s, in line with other advanced economies).

{kind=link}

Further, even if this was not true and U.S. corporate rates were actually higher than corporate rates in peer countries, there would still be no serious economic case that rate cuts would help low- and middle-income families, either by boosting “competitiveness” or through any other channel.

Economic policy changes can benefit the broad middle-class through three channels: lowering inequality by increasing the share of total income (including post-tax income) accruing to the middle-class, creating jobs, or boosting productivity (how much income is generated in an average hour of work in the economy). Corporate income tax rate cuts are weak, or even perverse, policy on all three fronts.

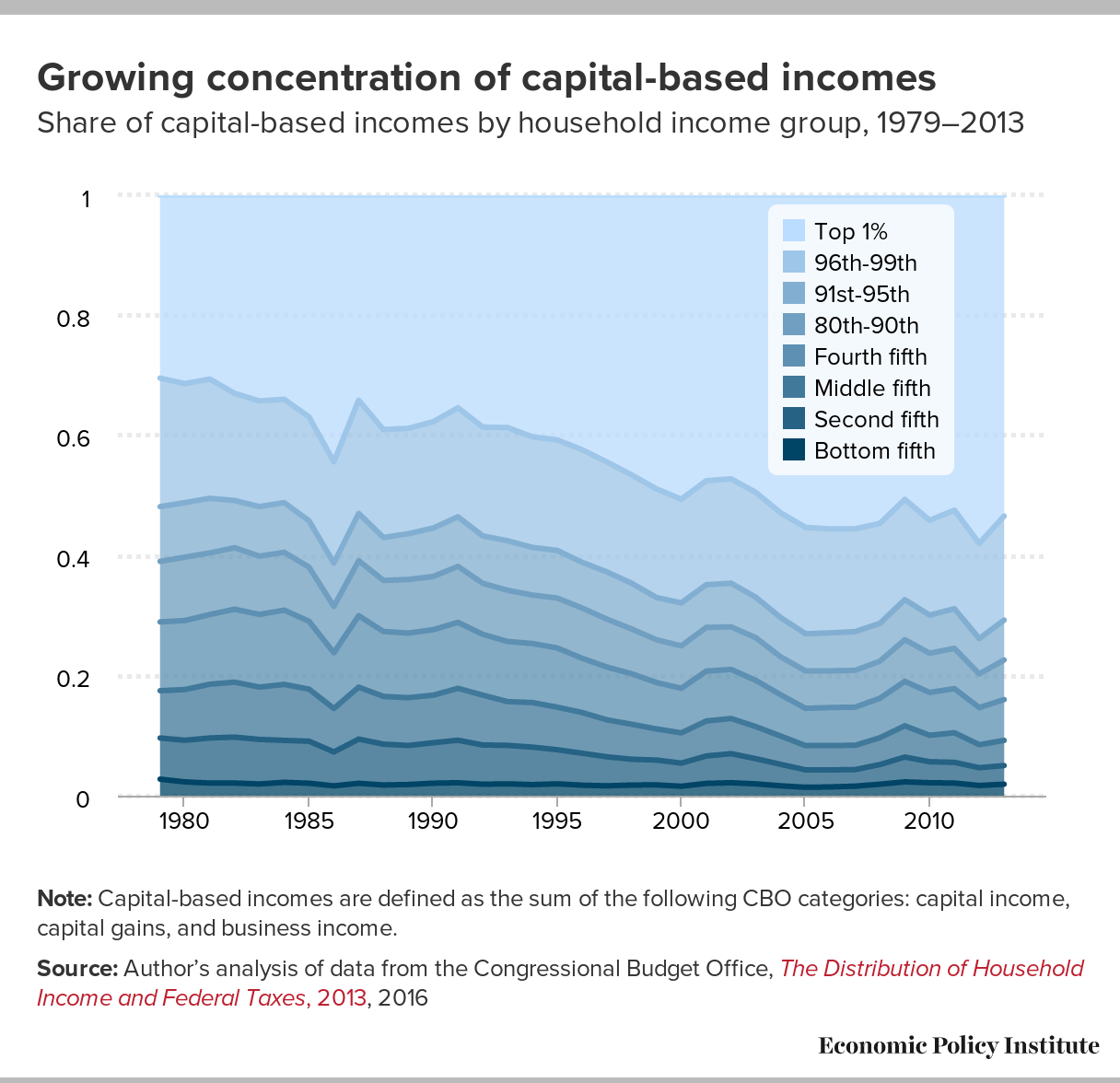

On inequality, the economic evidence clearly indicates that cutting corporate tax rates primarily benefits capital owners (corporate shareholders and business owners). And this capital ownership is extraordinarily concentrated at the top of the income distribution, with the top 1 percent claiming 57 percent of capital income, while the wealthiest 2 percent of households own 60 percent of all corporate equities. This means that the first-round effect of corporate rate cuts will be to shrink the share of post-tax income accruing to the middle-class, and to boost the share claimed by the very top.

{kind=link}

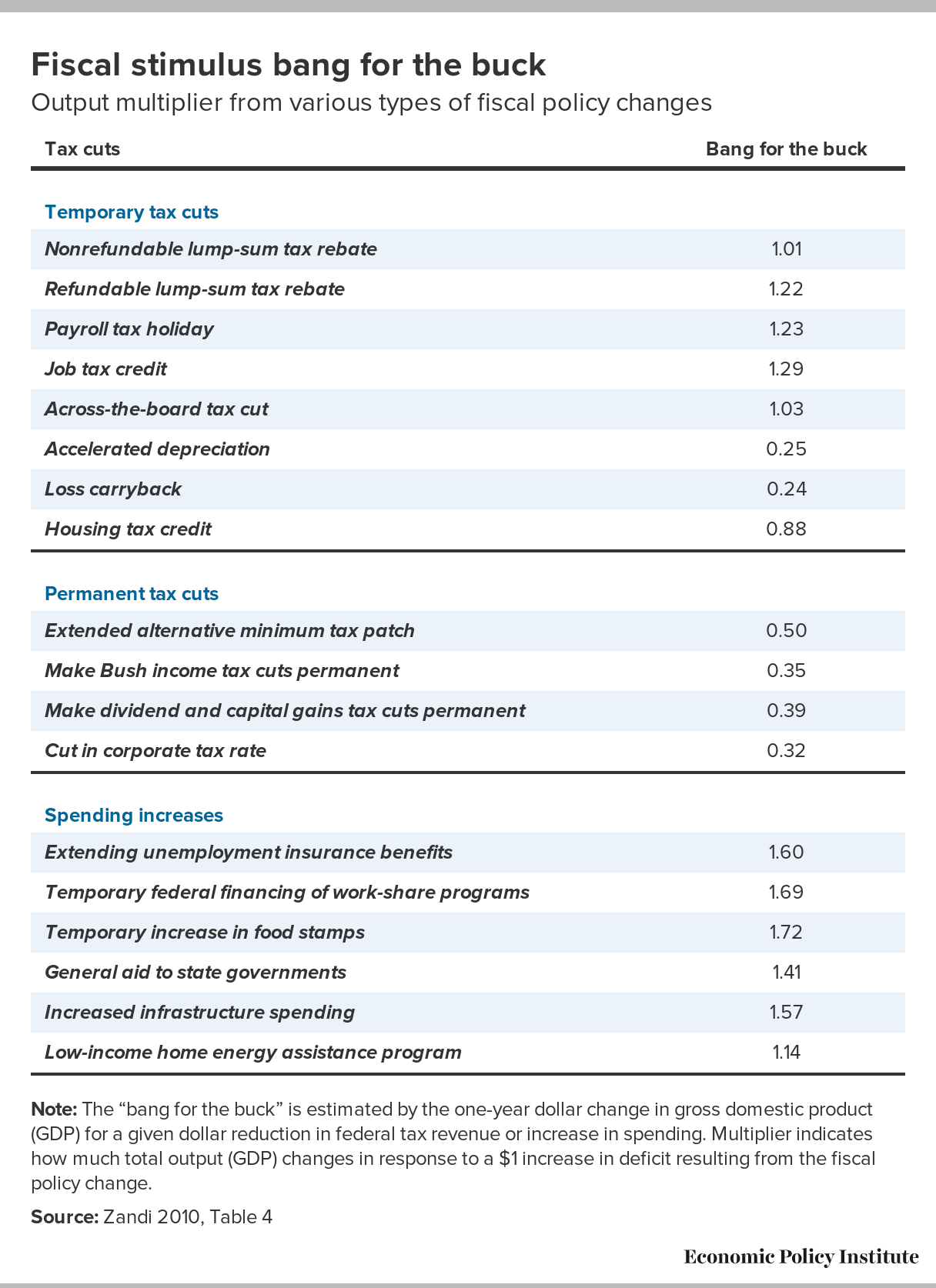

If job growth is currently constrained by too-slow economy-wide spending, then tax cuts could potentially help by boosting households’ post-tax purchasing power and inducing them to spend more. But compared to any other tax cut, in fact, corporate rate cuts induce very little additional spending. And each dollar spent in corporate rate cuts generates only about a fifth as much job growth as a dollar in additional government spending. The reason why corporate rate cuts only weakly boost spending is obvious: The benefits accrue mostly to already-rich households, whose spending is not constrained by their current income. Expanding tax cuts aimed at lower- and middle-income households, like the Earned Income Tax Credit (EITC), or boosting government spending are far more effective as job-creation tools.

{kind=link}

If job growth is not currently constrained by too-slow spending, then corporate rate cuts could, in theory, boost productivity. The textbook argument is that these cuts boost post-tax profits, which then translates into higher returns to owning stocks or bonds. These higher returns induce households to spend less and save more, and this increased supply of savings pushes down the cost of borrowing, or interest rates. Lower interest rates then allow firms to borrow more to finance new plants and equipment, and this raises productivity by giving workers more and better tools to work with.

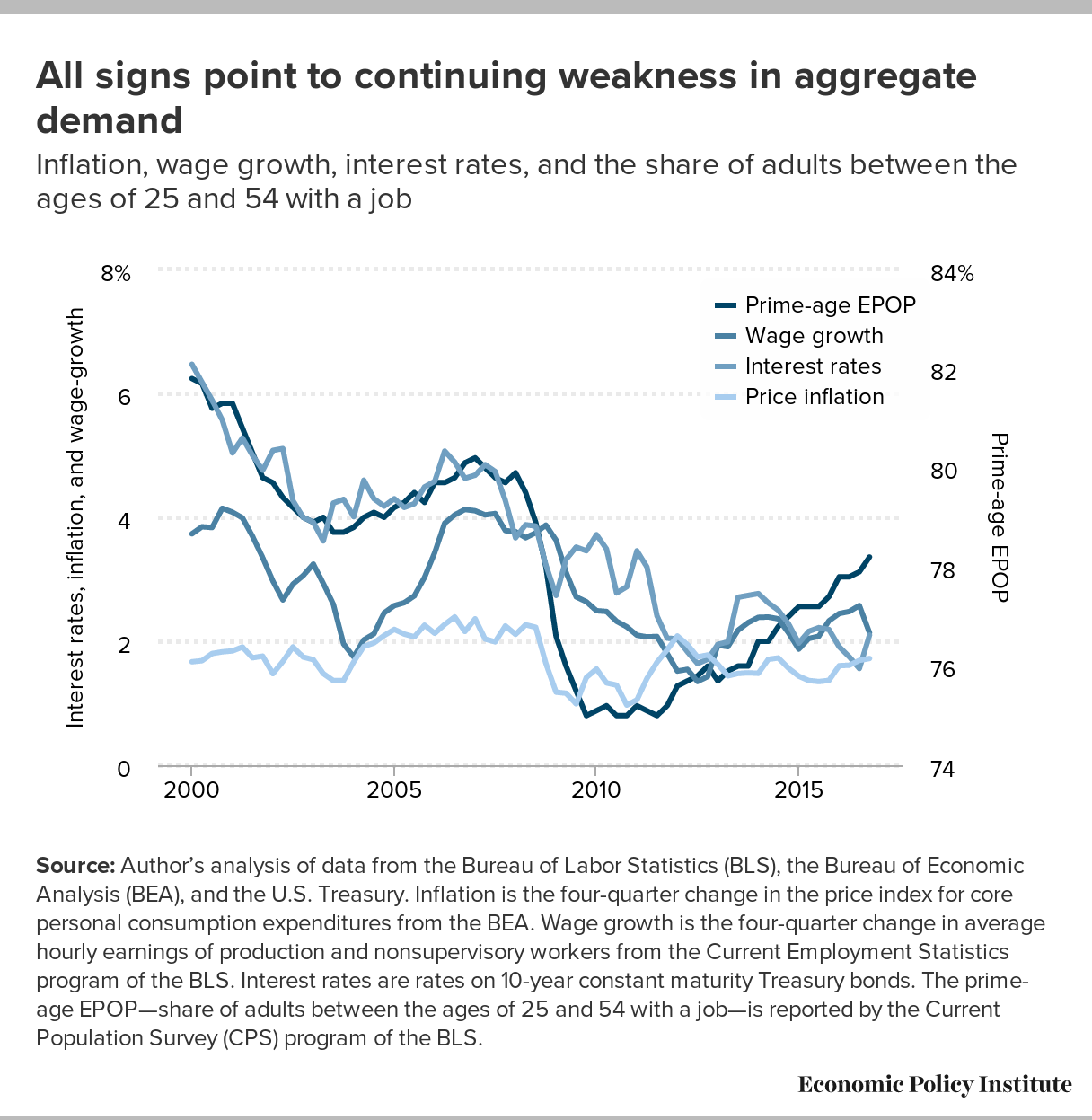

But today’s real-world data indicate strongly that no link in this happy chain of events will happen. First, if the most binding constraint on economic growth today is a shortfall of spending, then a corporate rate cut that boosted savings and reduced consumption would actually slow growth. There is ample evidence that this spending shortfall is indeed the most pressing constraint on growth. Evidence that it is spending, and not savings, that is in short supply today and should be addressed by policy can be seen in today’s still historically low interest rates, which have been depressed for years due to savings gluts, both domestic and global.

{kind=link}

{kind=link}

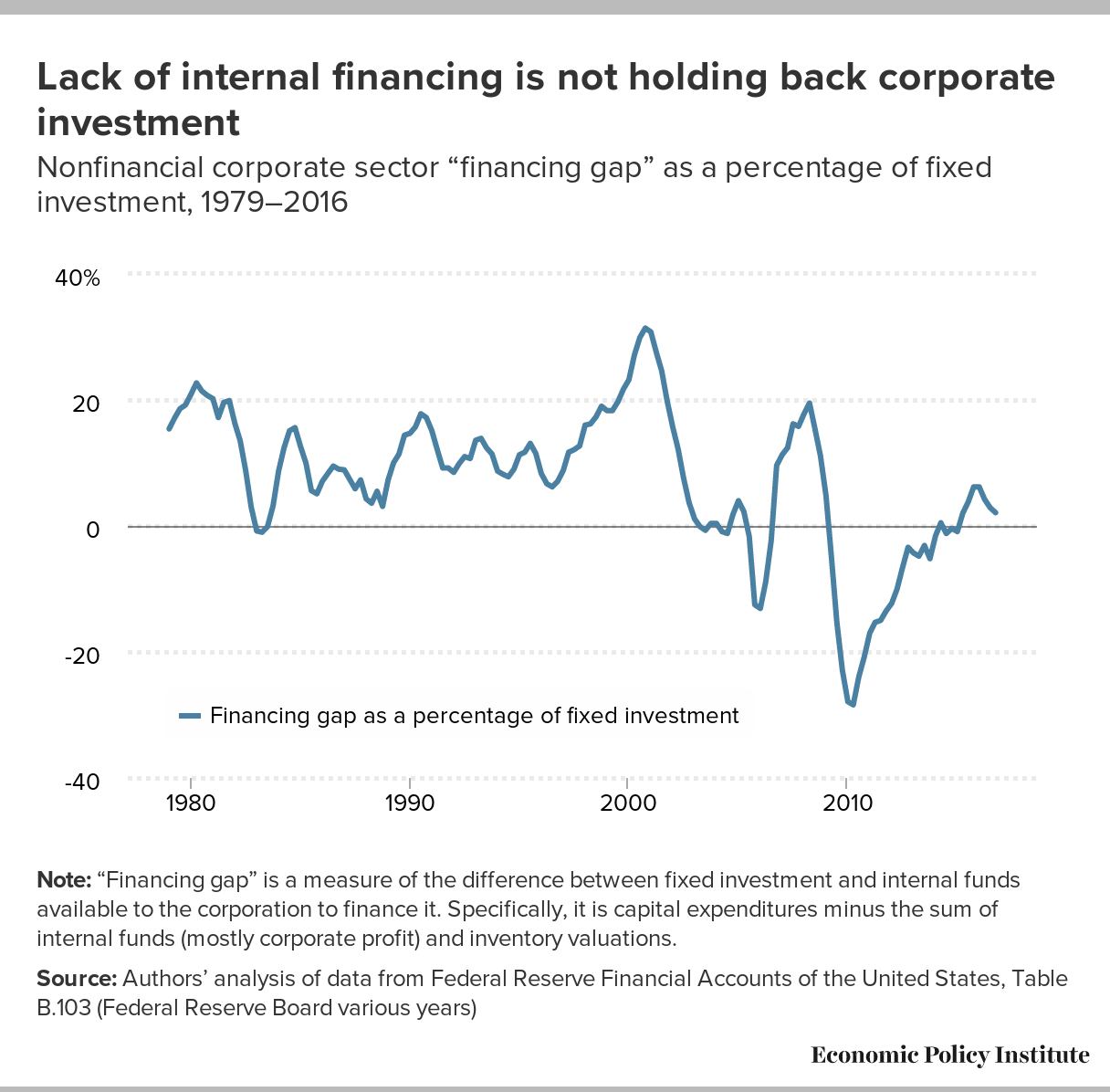

In fact, firms in recent years could finance all desired investment in plant and equipment with internal funds (i.e., retained earnings) without borrowing at all.

{kind=link}

Additionally, interest rates are affected by total national savings, which are the sum of private and public savings. While corporate rate cuts might boost private saving by inducing households to save more, they actually mechanically reduce public saving by increasing the federal budget deficit. This means that unless these tax cuts are paired with spending cuts or tax increases somewhere else, they fail even on their own terms because they will not boost national savings as a whole.

Finally, even if this all somehow worked out and a boost to savings reduced interest rates and business investment responded so that productivity did indeed rise, this would not guarantee the indented result. In recent decades, productivity growth has failed to boost wages for the bottom two-thirds of workers and has instead overwhelmingly just been claimed by a narrow slice of corporate managers and capital owners at the top of the income distribution.

All of this indicates that corporate rate cuts are either a flimsy or outright damaging tool with which to try to benefit typical American workers, as they increase inequality, only weakly support job growth, and are unlikely to deliver any boost to productivity.

Where does “competitiveness” fit into all of this? Well, nowhere, it’s a talking point, not an argument.

Some might think that U.S. companies will open factories abroad rather than domestically if post-tax profits are higher in other countries. But the United States taxes profits domestically and abroad at the same rate, so cutting this rate will boost post-tax profits equally, providing no “competitive” benefit.

But if profits are taxed the same here and abroad, why have American firms like Apple and Google and Facebook and Pfizer intentionally parked trillions of dollars in profits offshore? That’s because of a huge loophole in corporate taxes known as deferral.

Firms only need to pay taxes when their profits are repatriated to owners in the United States. And so long as there’s hope that Congress will give these offshore profits a “holiday” some year soon and allow them to be returned without paying their full tax rate (which is what happened in 2004), these profits will remain offshore.

The simplest solution to U.S. profits accumulating offshore is simple: Don’t cut rates, just end deferral and demand that these corporations pay their taxes when their income is earned, the same way you and I do.

Because deferral option is by far the single biggest loophole in the corporate tax code, plans that do not wrestle with this problem just seem unserious about base-broadening reform. The “Big 6” proposal does not just lack any detail on corporate loophole closing, it essentially makes the deferral loophole permanent. In the jargon of tax policy, it calls for switching the U.S. corporate code to a territorial system, taxing only economic activity within the borders of the United States. The profits of U.S.-owned companies’ offshore subsidiaries would no longer be taxed at all under a territorial system. Essentially, it takes today’s deferral loophole and makes it a permanent feature of the U.S. corporate code.

It’s worth noting that territorial could be paired with measures to stop the financial engineering that allows profits to appear on paper that have been made in obvious tax havens like the Cayman Islands or Ireland. Tax experts like Kimberly Clausing and Reuven Avi-Yonah, for example, note that we could assume profits are simply proportional to sales in their distribution across countries, and tax them accordingly. These would make the accounting gimmicks to move profits moot (sales are much harder to move on paper between countries). But nothing in the plan released last week gave any indication that the move to a territorial system was anything but a gambit to further lower the tax bill of American corporations.

The most obvious problem with our corporate tax system is that it raises too little from our corporate sector. Given this, it becomes clear that rate reductions will do next to nothing to boost typical American living standards. This, along with the permanent legalization of the most expensive loophole in our corporate code, is a terrible place to start this debate.

Click to

View Comments